The Era of Decarbonization and What it Means to Large Energy End-Users in Mexico

Climate change is widely regarded as the number one issue the world is facing as it has a profound socioeconomic impact. The effects of climate change are currently visible; for example, droughts are happening more often and are becoming more severe and so are the cold snaps, e.g., Texas Freeze.

It is important to mention that the pressure to act on climate change is being driven by governments, investors, companies, and the global society. Governments are just channeling and putting in place significant and coordinated efforts to reduce greenhouse gas emissions (GHG) and promote sustainable development scenarios (SDS), while investor are looking at organizations that embrace smart ESG (environmental, sustainable and governance) policies. The UK and the European Union (EU) were some of the first governing bodies to announce a strategy to achieve climate neutrality by 2050 with many countries following these footsteps and setting their own net-zero agendas. More significantly, China recently announced a strategy to achieve carbon neutrality by 2060 in December 2020.

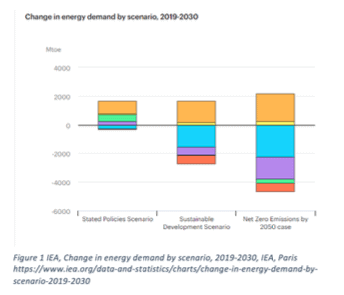

It is widely accepted that a far-reaching set of actions will be required to meet the ambitious targets set in these netzero agendas. It is unquestionable that unprecedented changes will take place to reduce GHG emissions, let alone push for the transition into a net-zero society through regulatory changes as well. These changes will affect the way we produce and consume goods and services as well as how we generate and consume energy. In this context, some experts have even indicated that the decarbonization process may have a far greater impact than the industrial revolution. For example, the International Energy Agency (IEA) indicated in its 2020 World Energy Outlook report that CO2 emissions from the power sector must decline by circa 60% between 2019 and 2030 with the share of renewable generation in the global electricity supply growing by 33% to 60% in the same time span.

The challenges to accommodate such a considerable increase in renewable generation combined with the reduction or even full elimination of fossil fuel power generation are significant. One of these challenges is the approach countries will take to substantially change its electricity generation mix to meet net-zero objectives. Some countries will rely on natural gas to make that transition and to provide stability to the grid whereas some other countries are betting on new regulatory reforms, new technologies and fuels such as hydrogen as a long- term solution for their baseload generation. For example, EU’s estimate is that at least 15% of the energy will have to come from green hydrogen by 2050 to meet the net-zero targets. A second challenge is to maintain grid stability to deal with the variability of renewable generation. The implementation of micro-grids, the redesign or reconfiguration and maintaining an adequate level of investment in the transmission and distribution network will be key elements to maintain grid stability in the short, medium, and long-term.

The impact of decarbonization on end-users, in particular large energy consumers, is quite significant, because they will have to calculate their direct and indirect emissions1, and put the necessary policies, and investments in place to reduce these emissions. Emission reduction will come at a cost. A 2018 McKinsey report on decarbonization of industrial sectors estimated that the cost of decarbonization of the production of cement, steel, ammonia, and ethylene would cost 21 trillion USD through 2050. It should not come as a surprise that the estimated cost of decarbonizing other industries such as the food and auto manufacturing would also be astronomical. These decarbonization costs arise from adopting new production or manufacturing techniques, and the installation of new equipment amongst others.

It is worth noting that large end-users may face additional costs related to decarbonization. For example, greater transmission and distribution charges to finance adequate levels of investment on the grid. However, large energy users must also consider the cost of complying with new regulations aimed at advancing net-zero policies.

These new regulations may come in the form of the so-called “carbon taxes”, stricter packaging standards and higher renewable goals.

One of these new possible pieces of regulation is the implementation of a “carbon border tax”. What is a carbon border tax? A carbon border tax is a type of import tax imposed on products generated in countries with less stringent climate and environmental policies. The objective of this carbon border tax is two-fold. The first objective is to protect the industry of the country enacting this carbon tax by disincentivizing companies moving production way from this country and preventing carbon leakage; and second, to incentivize climate policies similar in ambition to this country’s goals. In addition, a carbon tax will also cover those industries not covered by any emission cap-and-trade system (ETS) already in place.

The imposition of carbon border taxes will certainly have an impact on companies operating in many developing countries, for example Mexico. Many developing countries still rely on oil and coal for most of their electricity generation and are quite adamant on setting strict climate policies or targets not to curb economic growth. The hope is that these countries will experience a real economic impact for not embracing energy transition and decarbonization.

Some argue that levying a carbon tax should be a measure of last resort and that countries or economic blocks should incentivize the development of domestic and/or regional carbon emissions markets to help achieve emissions reduction targets. Emissions markets are based on the premise of having a cap on the number of emissions certificates to ensure that the desired/required emissions reduction targets will take place. In addition, the carbon price stimulates the innovation for clean technology and low-carbon drivers of economic growth.

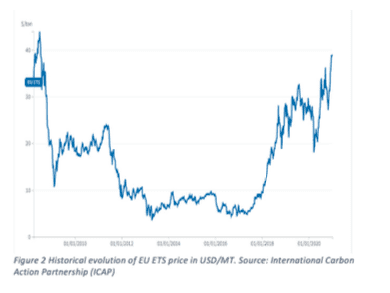

The development and implementation of these carbon emissions markets seem to be the preferred route because these markets are viewed as an efficient way to price carbon through the creation of supply and demand. Refinitiv recently estimated the total collective value of the global carbon emissions markets in 2020 was circa 270bn USD. The value of the emissions markets is expected to increase even further as more large end-users access them to achieve their emissions reduction targets and more markets become fully functional. EU, Switzerland, New Zealand, California, Quebec, Kazakhstan, and South Korea are some of the jurisdictions with fully functioning ETS markets. Trading in China’s ETS market is expected to start in the second quarter of this year and this market will become the largest emissions market in the world surpassing EU’s ETS market. Many other countries such as Mexico, Ukraine, and Colombia are in different stages of development of their own emissions markets.

It is quite clear that decarbonization is upon us and will become mandatory sooner rather than later as more countries start developing and implementing their own net-zero agendas. However, large end-users and their Boards must act on climate risk while preserving margins and remaining competitive. Let us take the food industry, for example. The food industry, particularly the meat industry, must take a decisive action to reduce its carbon emissions, which some estimate at 13.7 bn metric tons per annum, while keeping supplies and costs down as food inflation is a big issue around the world.

Large end-users must be ready to face the additional regulations and increases in costs associated with decarbonization. Therefore, large end-users and their leadership teams must start planning to get ahead of the challenges posed by national and global decarbonization standards. This planning process must consider two key aspects. The first aspect consists of the features that a large end-user can control or have a direct influence on. Having a reasonable supply chain, being efficient in their processes and energy consumption are some aspects that large end-users have direct control of and can be used to lower carbon emissions. From an energy consumption perspective, the path to decarbonization comprises of energy efficiency, full electrification, and process optimization. It is worth noting that energy efficiency programs lead to improved operations and better process controls. Another important factor regarding energy consumption is for companies to have a better understanding of the electricity market in their respective jurisdictions.

This understanding of the electricity market will help companies to devise a comprehensive action plan for a sustainable and cost-effective electricity supply model. In this context, many large end-users are currently exploring a decentralized electricity supply model which, in some cases, combines renewable on-site generation with a traditional electricity supply contract. The second type will be driven by regulation, consumers trends and shareholders. End-users must be agile, adaptable, and innovative to tackle the challenges presented by these stakeholders in the fight against climate change and emissions reduction targets.

In summary, decarbonization is a very complex, costly and important issue that will dominate the political and economic discussions for the foreseeable future. The stakes are very high with many significant challenges and unknowns ahead for businesses, investors, and consumers. Decarbonization challenges are not insurmountable but it will require a great and concentrated effort from business leaders to plan for and anticipate these changes. If you are a large end-user, it will require incredible support and commitment to achieve the ambitious emissions reduction targets that are unfolding as you read this article. If you are in the C- suite, you do not have to be a visionary to realize your business plans should already consider these factors and the inclusion of various advisors that can help you navigate the changes currently unfolding.

Source:

1 Direct emissions are those originated from sources owned or controlled by an end-user whereas indirect emissions are generated as a consequence of an end-user’s activities.